Electrons Can't Fix a Molecule Problem: India's Pain When Oil Crosses $100

India's energy transition is not just an electricity story—solving industrial heat, heavy transport, and fuel dependence requires clean molecules as much as clean electrons

.jpg)

The electricity problem is already being solved. The fuel problem isn’t.

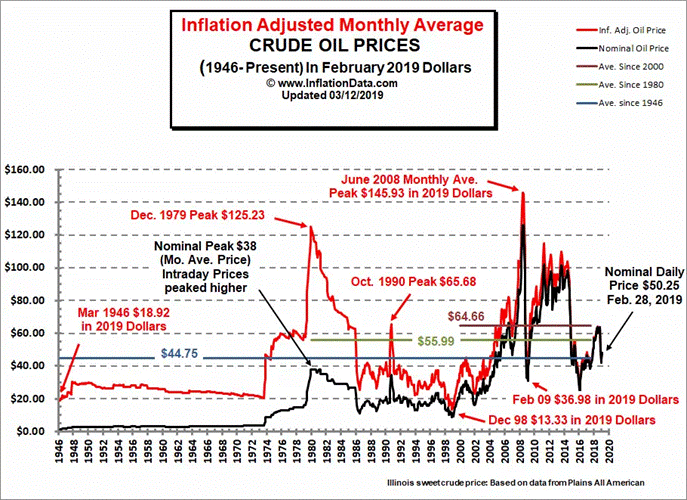

Brent is above $100. The Strait of Hormuz is effectively closed. India, which imports roughly 85 per cent of its crude, is watching its import bill balloon by nearly $48 a barrel in twelve months. We have been here before: 1979, 1990, 2008, 2011 to 2014, 2022. Every time, the window for alternatives has closed before India acted decisively.

This time has to be different, not because the crisis is worse, but because the structure of the energy problem has changed. The Same Playbook, the Same Inaction

India’s response to oil shocks follows a painful pattern. In 1979, administered pricing insulated consumers but gutted the fiscal balance. In 1990, India pledged gold reserves to the Bank of England. In 2008, the petroleum subsidy bill crossed ₹1 lakh crore and the National Biofuels Policy was announced, though implementation was almost non-existent. In 2022, ethanol blending accelerated, but industrial fuel switching did not.

{kind=link}

Crisis leads to coping, not transformation. Each time, India managed the fiscal impact through subsidies, pricing reform, and opportunistic Russian barrels, without building the structural alternatives that would make the next shock less damaging.

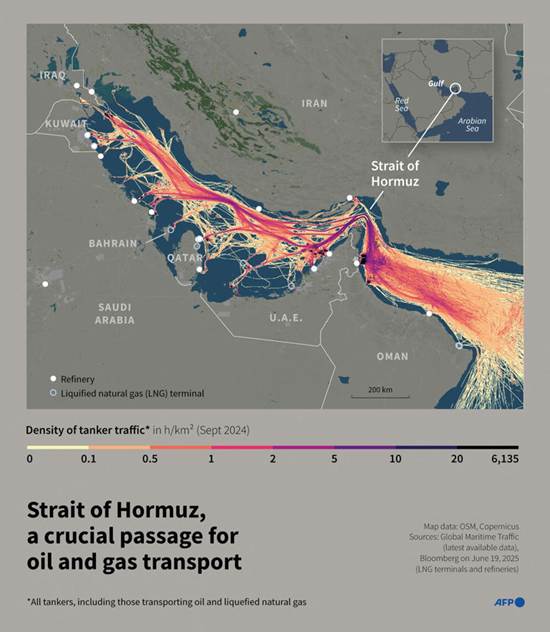

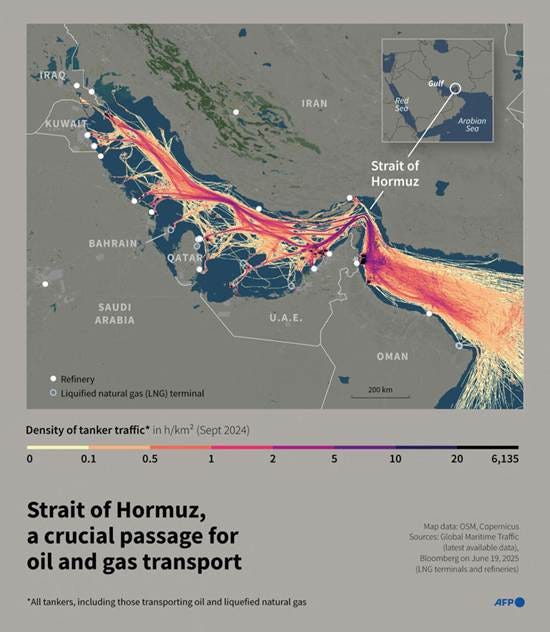

Hormuz Is Not a Quick Fix

The strait is 33 kilometres wide at its narrowest. Roughly 20 million barrels, a fifth of global consumption, pass through it daily. With it now effectively closed, rerouting takes years, not weeks. Tankers around the Cape add 10 to 15 days and $3 to $5 per barrel. Bypass infrastructure is a five-to-ten-year build. India must plan for a prolonged period of elevated and volatile oil prices.

Energy Is Three Problems, Not One

Every unit of useful energy India consumes falls into one of three buckets:

Electricity: electrons through wires. Lighting, computing, motors, AC, and increasingly transport. It can come from any source.

Molecules: chemical fuels that store energy in bonds. Petrol, diesel, ATF, LPG, gas, ethanol, biodiesel, biogas, hydrogen. Used wherever energy must be stored, moved without wires, or combusted.

Heat: direct thermal energy for industry. Cement kilns at 1,450°C, steel reheating at 1,200°C, textile dryers at 150 to 200°C. The source, whether burning molecules, electric resistance, or concentrated solar, drives cost and feasibility.

The central error in India’s energy discourse is treating these three as one problem. They are not. Different physics, different economics, different supply chains. Get the strategy right, solve each separately, and then see where they connect.

Electricity Is Getting Solved, Faster Than Most Realise

Two forces are converging.

Wright’s Law. For every doubling of cumulative production, unit costs fall by a consistent percentage. Solar modules have followed a learning rate of around 24 per cent. Utility-scale solar in India cost ₹12 to ₹15 per kWh in 2010; by 2024, winning bids were below ₹2.50. Lithium-ion batteries followed the same trajectory, dropping from over $1,100 per kWh in 2010 to under $140 per kWh in 2024. This is structural, not cyclical. No OPEC decision, no Hormuz closure can reverse it.

Kalpakkam. In April 2026, the 500 MWe Prototype Fast Breeder Reactor reached first criticality after a decade in the making. It produces more fissile material than it consumes and serves as the bridge to India’s thorium reserves. India is now only the second country after Russia with a commercially operating FBR. The target is nuclear at around 25 per cent of generation by 2047.

The caveat matters. Kalpakkam is a prototype, and scaling from one reactor to a fleet takes years. Grid build-out takes longer. Electricity’s long-term trajectory is secure; its near-term supply is not. But the direction is clear: solar and wind for variable generation, nuclear for carbon-free baseload. The electron problem has a credible path. The molecule and heat problems do not.

The Real Gap: Molecules and Heat

If electricity is increasingly handled by renewables and nuclear, the real policy gap is not electrons. It is fuel.

Wright’s Law does not apply to molecules the way it applies to electrons. A solar panel is a manufactured product that rides factory learning curves. A litre of diesel is an extracted commodity whose cost is set by geology, geopolitics, and logistics. Biofuels sit in between. The conversion technology, including gasification, fermentation, and anaerobic digestion, does benefit from learning, but the feedstock is agricultural, seasonal, and distributed. Biofuels will not follow solar’s exponential curve, and they do not need to. They only need to beat imported fossil fuels at $100 oil, and they already do.

The sectors where India remains exposed to imported hydrocarbons are precisely the sectors that electricity cannot easily reach:

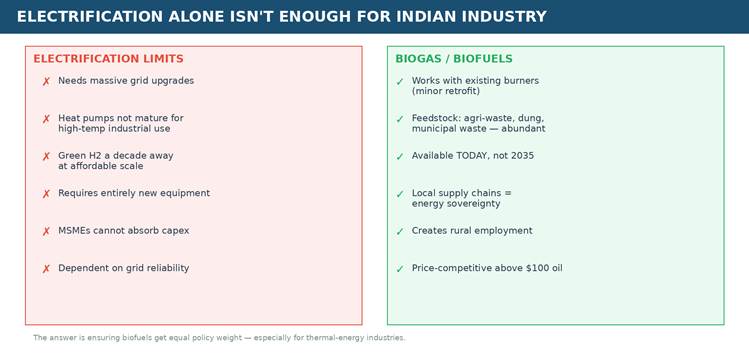

Industrial process heat. Cement kilns, steel reheating, textile dryers, brick kilns, and chemical reactors. Electrification is possible in some cases but expensive and grid-constrained. Here, electricity is not a bystander; it is a genuine competitor to biofuels, and green hydrogen is a third pathway. But note what green hydrogen actually is: a molecule generated from green electricity. Replacing fossil molecules with green ones requires enormous amounts of cheap, clean power we do not yet have. In the near term, at Indian grid prices and current electrolyser economics, biomass and CBG win on cost.

Transport segments that cannot electrify quickly. Long-haul trucking, agricultural machinery, and more than 700,000 telecom towers running diesel gensets.

Off-grid and distributed power. Diesel gensets across rural India, construction sites, and small commercial units, all running on imported molecules.

Why $100 Oil Flips the Calculation

Below $70 to $80, switching industrial fuel systems is hard to justify. Capex on new boilers and burners does not pay back fast enough. Above $100, the breakeven flips. Biogas, CBG, biodiesel, ethanol blends, and direct electrification of certain thermal loads start competing on unit economics, not ideology.

Brent went from $61 in January 2026 to over $118 by the end of Q1, the largest inflation-adjusted quarterly jump since 1988. This is the moment that matters, not as a talking point, but as a window for capital decisions that will lock in fuel systems for 15 to 20 years.

India’s Accidental Advantage: The Gas Road Not Taken

Most industrialised economies built out natural gas alongside electrification. Pipelines embedded into clusters and created decades of dependency. India’s gas push underperformed, and that failure is now an advantage.

India targeted raising gas from around 6 per cent to 15 per cent of its energy mix. Pipelines lagged, domestic production underwhelmed, and industrial adoption was patchy. The irony is that this gap can be filled by biogas. A ceramics cluster in Morbi or a textiles hub in Surat that never received a gas pipeline can leapfrog straight to CBG.

The window is time-limited. As PNGRB’s CGD networks expand, industrial users are being connected to piped gas. Once they invest in gas-fired equipment and sign long-term supply deals, the switching cost to biogas rises sharply. The biofuel leapfrog is a one-time advantage that erodes with every new pipeline commissioned.

Match Each Industrial Need to the Right Domestic Fuel

Dissociate the problem:

Biogas and CBG replace natural gas. The feedstock is local (agricultural residue, cattle dung, municipal waste), the technology is proven, and at $100-plus oil the economics are compelling.

Ethanol and biodiesel replace diesel. Ethanol blending has been a success story, but its potential extends well beyond petrol. India’s 700,000-plus telecom towers run on diesel gensets; at $110 crude, the telecom diesel bill alone is in thousands of crores annually. Ethanol gensets and biodiesel blends directly displace that demand. The same logic applies to railway diesel, agricultural pump sets, and commercial vehicle fleets.

Biomass pellets, briquettes, and co-firing replace coal in process heat. For brick kilns, cement pre-calciners, small foundries, and co-firing in existing boilers, compressed biomass is a direct drop-in. India’s surplus agricultural residue, over 750 million tonnes annually and much of it burned in fields, is the feedstock base.

The Feedstock Competition Problem

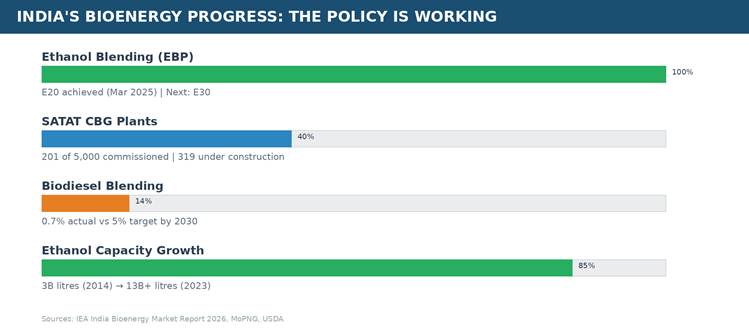

SATAT, which targets 5,000 CBG plants, is the right instinct. More than 200 are commissioned and over 300 are under construction as of early 2026. But there is a harder question: every biofuel programme is competing for the same resource base. Crop residue targeted for CBG is the same residue claimed by 2G ethanol, biomass power, biochar, pellet exports, and now co-firing mandates. Cattle dung is contested by biogas, organic fertiliser, and traditional use.

Without a national feedstock allocation framework, biofuel programmes will cannibalise each other, driving input costs up and leaving all of them subscale. India must map the total available biomass by type and geography, assign priority end-uses for each stream, and prevent policy-driven competition between programmes chasing the same inputs.

The Industrial Buyer Wants Predictability, Not Blending Targets

An MSME food processor in Maharashtra or a textile dyer in Tamil Nadu does not care about national blending targets. They care about whether they can sign a five-year fuel supply agreement at a price they can model into a cost sheet.

The practical agenda:

1. Cluster-level planning. Map industrial clusters (Surat textiles, Morbi ceramics, Tiruppur dyeing, Ludhiana engineering) to feedstock within a 50 to 100 km radius.2. Standardised off-take contracts with price-escalation formulae tied to a transparent index.3. Viability gap funding for small-diameter pipelines, local storage, and metering.4. A feedstock allocation framework that prevents cannibalisation.5. A policy signal that bioenergy is a permanent part of India’s energy architecture, not a transitional stopgap.

The Window Is Open. Act Before It Closes.

India’s industrial sector is at an inflection point. The companies that lock in their fuel systems in the next three to five years will operate them for decades.

The electron problem has a credible path: solar on the learning curve, nuclear arriving behind. What remains unsolved is the molecule problem. The worst outcome would be to treat this as another crisis to be managed and forgotten. The best outcome would be to use this moment to build the bioenergy infrastructure that makes the next oil shock irrelevant to Indian industry.

{kind=link}